“We had insurance… or at least we thought we did.”

Ramesh had built his logistics business from scratch.

Ten years of sleepless nights, late deliveries, tight margins — and finally, his company had begun handling high-value electronic consignments for regional distributors.

Every shipment felt like progress.

Every delivery meant trust.

So when he signed a Marine Cargo Insurance Policy, he felt relieved.

“अब टेंशन क्या है? Insurance hai,” he told his team confidently.

But what happened one rainy night on a highway outside Nagpur changed everything.

🚚 The Night That Changed Everything

It was a routine transit.

A truck carrying **₹12 lakh worth of electronic goods** — LED panels, routers, and accessories — left the warehouse at 2 AM. By dawn, it was supposed to reach the distribution hub. But halfway through the journey, the driver stopped for tea.

Ten minutes.That’s all it took. When he returned, the back shutter was broken open.

Half the cargo — gone.

No CCTV.

No witnesses.

Just silence… and panic.

The police complaint was filed immediately.

The client demanded answers.

And Ramesh did what he believed would save him.

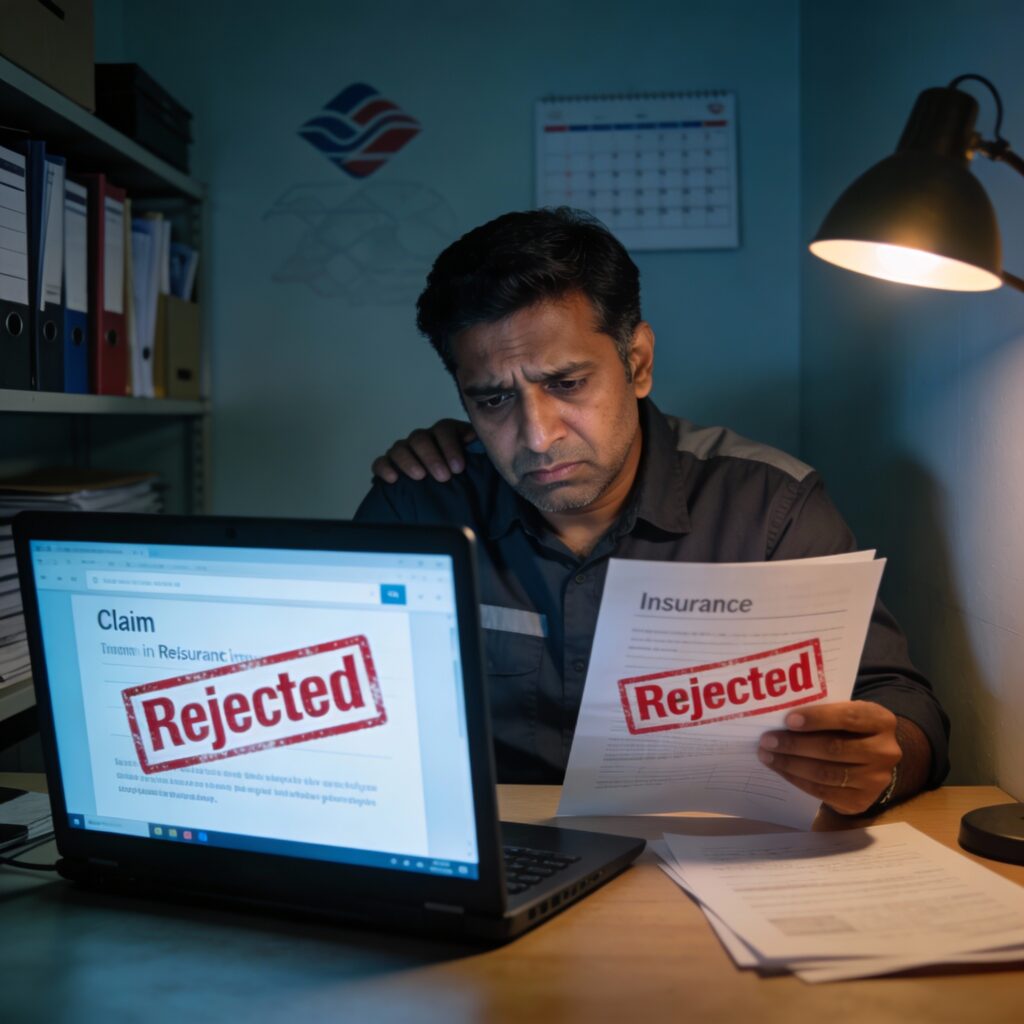

👉 “He filed an insurance claim.”

❌ The Shocking Reality: “This Is Not Covered”

Two weeks later, the insurer’s response arrived.

“Claim Rejected.”

Reason:

“Policy covers goods only while stored inside the insured warehouse. Transit risk is not included.”

Ramesh couldn’t believe it.

He argued.

He pleaded.

He showed invoices and FIR copies.

But the policy wording was clear.

✔️ Warehouse – Covered

❌ Transit – Not Covered

The ₹12 lakh loss came straight from his pocket.

No reimbursement.

No compensation.

No second chance.

💔 The Real Damage Wasn’t Financial

The money hurt — yes.

But what hurt more was:

- The client lost trust

- Future contracts were paused

- Cash flow collapsed

- EMIs piled up

- Staff salaries got delayed

All because of – One assumption:

“Marine insurance automatically covers transportation.”

It doesn’t.

⚠️ The Most Common Misunderstanding in Marine Insurance

This is where most businesses go wrong.

They hear “Marine Insurance” and assume:

✔ Goods are covered

✔ Transit is included

✔ Theft is protected

✔ All risks are insured

But in reality:

🔴 Warehouse-only policies exist

🔴 Transit needs separate coverage

🔴 Route, mode, and distance matter

🔴 Loading/unloading risks are optional add-ons

And unless your policy clearly mentions:

* Transit cover

* Mode of transport (road/rail/sea)

* Start & end points

* Type of goods

* Theft & pilferage clauses

👉 You’re exposed.

📉 The Cost of Assumption vs. Cost of Awareness

Ramesh paid ₹18,000 for his insurance policy.

He lost ₹12,00,000 because he didn’t read:

* Scope of cover

* Exclusions

* Transit clause

That’s a ₹11.82 lakh lesson* in fine print.

✅ What Could Have Saved Him?

A properly structured Marine Transit Policy that included:

✔ Door-to-door transit coverage

✔ Theft & pilferage protection

✔ Coverage during loading/unloading

✔ Route-based risk assessment

✔ Correct sum insured

✔ Declaration-based policy for regular movement

Most importantly — “expert guidance before buying.“

🔍 The Bigger Lesson for Every Business Owner

If your business involves:

- Logistics

- Manufacturing

- Wholesale

- E-commerce

- Distribution

- Electronics

- FMCG

- Machinery

Then “transit risk is your biggest blind spot.“

And insurance bought in haste becomes regret in crisis.

💡 Final Thought

Insurance doesn’t fail people.

“Misunderstanding does.“

Before your next shipment leaves the warehouse, ask yourself:

👉 “If this truck disappears today, will my policy really pay?”

If you’re unsure — that’s your warning sign.